This was Treasurer, Dr Jim Chalmer’s first budget and the first for the Labor government since winning the election in May this year. The government came to power against a backdrop of the economic disruption and commodity-driven inflationary pressures stemming largely from the Covid-19 pandemic and the war in Ukraine, with anemic wage growth, skills shortages, underemployment and energy costs rising out of control during the current transition from fossil fuels to renewable energy and natural disasters, to name a few.

If the market’s reaction to recently deposed UK Prime Minister Liz Truss’s economic plan for the UK based on spurring economic activity with further quantitative easing in a volatile and increasingly inflationary environment was any “how-not-to” guide for our newly minted government, they certainly heeded the message.

In his budget address, the Treasurer talked about some of the current global challenges and high inflation and laid out a plan built on “responsible, reasonable and targeted” economic management and “exercising fiscal restraint so as not to put more pressure on prices and make the Reserve Bank’s job even harder.”

So, we didn’t see any broad cash splash, which will leave a lot of people scratching their heads thinking, “how does this help me and my family with the cost-of-living pressures we’re all facing?” Instead, the Budget sets out a targeted 5-point plan for cost-of-living relief in the areas of childcare, expanding paid parental leave, medicines, affordable housing and wage growth.

There were also announcements in areas such as preparing for the referendum to enshrine a First Nations Voice to Parliament in the Constitution, funding 480,000 fee-free TAFE and community based vocational education places, increasing the maximum co-payment under the Pharmaceutical Benefits Scheme (PBS), further funding for the transition to cleaner energy (including a commitment to a national rollout of hydrogen refuelling and charging stations for hydrogen and electric powered vehicles), a $15 bn reconstructions fund to help address the devastation cause by the recent multiple east-coast flood events, commitment to continue addressing violence against women and children, veteran suicide, repairing the NDIS and preserving our military strength, among many others.

However, was there anything for individuals and businesses for tax, superannuation, social security or anything that we can really hang our hats on when looking at wealth creation and retirement funding strategies? Not really. Let’s look at the economic numbers first and decide who the winners and losers might be out of this budget.

The macro

Some good news is that while higher prices are impacting all of us, the government has picked up a handy $150 bn windfall in extra revenue from higher commodity prices. The budget deficit is actually $100 bn better than the forecast from the previous budget and while inflation is expected to peak at around 7.75% by Christmas, it is projected to moderate to 3.5% through 2023-24 and return to the Reserve Bank’s target range of 2.0% to 3.0% in 2024-25.

On the downside, the economy is expected to grow by 3.25% in 2022-23 but is then predicted to slow to 1.5% for 2023-24, lower than the 2.5% that was forecast in March.

The Budget estimates an underlying cash deficit of $36.9 billion for 2022-23 (and $44bn for 2023-24). Net debt projected in the March budget of $714.9 billion for 2022-23 and peaking at $864.7 billion (33.1%) in 2025-26, is reasonably better at $766.8 bn (28.5% of GDP) but borrowing is more expensive in a higher interest rate environment, so it doesn’t seem there was much wriggle room on any cash splash … pity.

The more relevant goodies (without the detail)

At a high level, this budget contained a range of very specific measures targeting taxation, superannuation, housing and social security but no wholesale tweaking or reforms that really enter conversations on wealth creation and retirement funding strategies. The following summary is not complete and focusses only on the specific taxation, superannuation and social security measures. Some of the following announcements are described in more detail further on in this report.

Taxation

• Personal tax rates remain unchanged for 2022-23 and the already legislated Stage 3 tax cuts starting from 2024-25 unchanged.

• Cryptocurrency is not a foreign currency – as governments around the world tackle with how to assess gains and losses on crypto, the Government will introduce legislation to clarify that digital currencies (such as Bitcoin) continue to be excluded from the Australian income tax treatment of foreign currency.

Superannuation

• Super downsizer contributions – the government confirmed that it will reduce the eligibility age to 55 (60 currently).

• SMSF residency changes – the proposal to extend the central management and control (CM&C) test safe harbour from 2 to 5 years, and remove the active member test, will now start from the income year commencing on or after assent to the enabling legislation (previously 1 July 2022).

• SMSF audits every 3 years – the Government will not proceed with the former government’s proposal to allow a 3-yearly audit cycle for SMSFs with a good compliance history.

• Retirement income products – the Government will not proceed with the proposal to report standardised metrics in product disclosure statements (PDSs).

Social Security and housing

• Affordable housing measures – the Government will establish a Regional First Home Buyers Guarantee Scheme and a Housing Australia Future Fund.

• Housing Accord – targeting 1 million new homes over 5 years from 2024. The Government will commit $350m over 5 years to deliver 10,000 affordable dwellings. The Accord has been struck between State and Territory governments and investors and will include super funds.

• Paid Parental Leave (PPL) scheme – to be expanded from 1 July 2023 so that either parent can claim the payment. From 1 July 2024, the scheme will be expanded by 2 additional weeks a year until it reaches a full 26 weeks from 1 July 2026.

• Childcare subsidy – maximum CCS rate to be increased from 85% to 90% for families for the first child in care and increase the CCS rate for all families earning less than $350,000 in household income.

More detail on a few of the measures

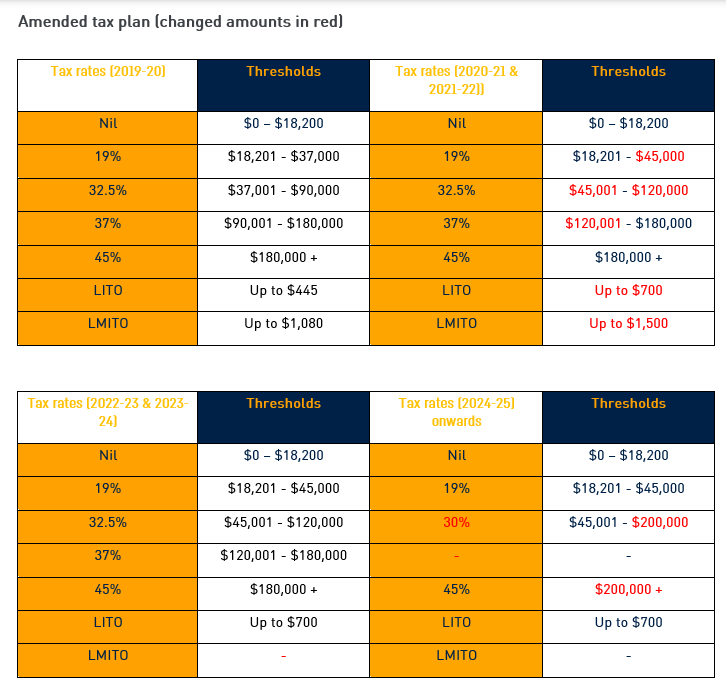

Personal taxation – Marginal Tax Rates

There were no changes to personal tax rates announced in this budget. The Government’s legislated three-stage tax plan that was announced in 2018 and enhanced in 2019 is as follows.

• Stage 1 amended the 32.5% and 37% marginal tax brackets over 2018-19 to 2021-22 and introduced the Low- and Middle-Income Tax Offset (LMITO);

• Stage 2 was designed to further reduce bracket creep over 2022-23 & 2023-24 by amending the 19%, 32.5% and 37% marginal tax brackets: and

• Stage 3 was aimed at simplifying and flattening the progressive tax rates for 2024–25 and increasing the Low-Income Tax Offset (LITO). From 1 July 2024, there will only be 3 personal income tax rates – 19%, 30% and 45%. The Government estimated that around 94 per cent of taxpayers would be on a marginal tax rate of 30% or less (as shown in the tables below).

Low- and Middle-Income Tax Offset (LMITO) is no more

The LMITO increased by $420 for the 2021-22 income year so that eligible individuals (with taxable incomes below $126,000) received a maximum LMITO up to $1,500 for 2021-22 (instead of $1,080).

There was no announcement in this Budget of any extension of the LMITO to the 2022-23 income year meaning the LMITO has effectively ceased and been replaced by the low-income tax offset (LITO) (described below).

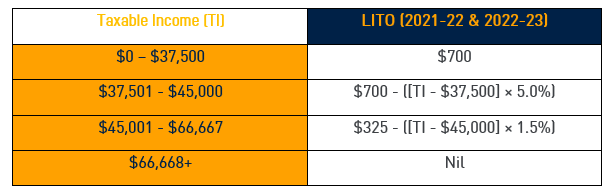

Low Income Tax Offset (LITO) for 2022-23 – unchanged

The low-income tax offset (LITO) will continue to apply for the 2021-22 and 2022-23 income years. The LITO was intended to replace the former low income and low- and middle-income tax offsets from 2022-23, but the new LITO was brought forward in the 2020 Budget to apply from the 2020-21 income year. The LITO will continue to apply for the 2022-23 income years and beyond.

Super downsizer contributions eligibility age reduction to 55 confirmed

The Government confirmed its election commitment that the minimum eligibility age for making superannuation downsizer contributions will be lowered to age 55 (from age 60). This measure will have effect from the start of the first quarter after assent to the enabling legislation – the Treasury Laws Amendment (2022 Measures No 2) Bill 2022 (introduced in the House of Reps on 3 August 2022).

The proposed reduction in the eligibility age will allow individuals aged 55 or over to make an additional non-concessional contribution of up to $300,000 from the proceeds of selling their main residence outside of the existing contribution caps. Either the individual or their spouse must have owned the home for 10 years.

As under the current rules, the maximum downsizer contribution is $300,000 per contributor (i.e., $600,000 for a couple), although the entire contribution must come from the capital proceeds of the sale price. A downsizer contribution must also be made within 90 days after the home changes ownership (generally the date of settlement).

Specific to the social security assessment of the proceeds from selling a principal place of residence, the Government also confirmed its election commitments that seek to assist pensioners looking to downsize their homes, by:

• extending the social security assets test exemption for sale proceeds from 12 months to 24 months; and

• changing the income test to apply only the lower deeming rate (0.25%) to principal home sale proceeds when calculating deemed income for 24 months after the sale of the principal home.

These measures are contained in the Social Services and Other Legislation Amendment (Incentivising Pensioners to Downsize) Bill 2022 (introduced in the House of Reps on 7 September 2022). The Bill will commence on 1 January 2023 (or 1 month after the day the Bill receives the assent).

Social Security and Aged Care

Paid parental leave to be expanded

The Government announced that it will expand the Paid Parental Leave (PPL) scheme from 1 July 2023 so that either parent is able to claim the payment and both birth parents and non-birth parents are allowed to receive the payment if they meet the eligibility criteria. The benefit can be paid concurrently so that both parents can take leave at the same time. From 1 July 2024, the Government will start expanding the scheme by 2 additional weeks a year until it reaches a full 26 weeks from 1 July 2026.

Sole parents will be able to access the full 26 weeks. The amount of PPL available for families will increase up to a total of 26 weeks from July 2026. An additional 2 weeks will be added each year from July 2024 to July 2026, increasing the overall length of PPL by 6 weeks. To further increase flexibility, from July 2023 parents will be able to take Government-paid leave in blocks as small as a day at a time, with periods of work in between, so parents can use their weeks in a way that works best for them. Further changes to legislation will also support more parents to access the PPL scheme. Eligibility will be expanded through the introduction of a $350,000 family income test, which families can be assessed under if they do not meet the individual income test. Single parents will be able to access the full entitlement each year. This will increase support to help single parents juggle care and work.

Businesses, particularly small businesses faced with ever-increasing energy and other costs will be disappointed with this budget. The government announced new integrity measures for off-market share buybacks, new anti-avoidance measures for significant global entities (SGEs), dropped a previously announced budget proposal from 2021-22 to allow taxpayers to self-assess the effective life of intangible depreciating assets and dumped a swathe of previously announced finance-related proposals and deferred a few more. But the government did announce new reporting requirements in the name of increasing tax transparency and also increased funding to the ATO (and the TPB) for tax compliance programs.

Probably the only measure of some relevance relates to businesses who benefitted from various State and Territory COVID-19 grant programs which the government announced would be eligible for non-assessable, non-exempt (NANE) treatment, which will exempt eligible businesses from paying tax on these grants.

Conclusion and where to from here?

Truth be told, this has been a very “unexciting” budget. There were no visionary reforms or even minor tweaks. The government had to face the hard task of what potentially irresponsible spending might do in a high-inflation environment and it has certainly chosen the more “responsible” and conservative route, which is the usual course for a government in its first term. It will be interesting however to see how the electorate responds in the face of crippling cost of living challenges, especially given the government came to power on a platform of “no one will be left behind”.

With inflation projected to moderate to 3.5% through 2023-24 and return to the Reserve Bank’s target range of 2.0% to 3.0% in 2024-25, and the net debt position on the improve, maybe we’ll see a bit more cheer as we get through the second and into the third term of government (some spending might go down well before the next election, if we can afford the electricity bill for our frozen dinners, TVs and Wi-Fi).

As with all budget announcements, the measures are proposals only and need to be enacted by Parliament.

I urge readers to contact your financial adviser with any specific questions you may have.

General Advice Warning

The information in this presentation contains general advice only, that is, advice which does not take into account your needs, objectives or financial situation. You need to consider the appropriateness of that general advice in light of your personal circumstances before acting on the advice. You should obtain and consider the Product Disclosure Statement for any product discussed before making a decision to acquire that product. You should obtain financial advice that addresses your specific needs and situation before making investment decisions. While every care has been taken in the preparation of this information, Infocus Securities Australia Pty Ltd (Infocus) does not guarantee the accuracy or completeness of the information. Infocus does not guarantee any particular outcome or future performance. Infocus is a registered tax (financial) adviser. Any tax advice in this presentation is incidental to the financial advice in it. Taxation information is based on our interpretation of the relevant laws as at 1 July 2020. You should seek specialist advice from a tax professional to confirm the impact of this advice on your overall tax position. Any case studies included are hypothetical, for illustration purposes only and are not based on actual returns.

Infocus Securities Australia Pty Ltd (ABN 47 097 797 049) AFSL No. 236 523.