The macro

The 2020-21 Federal Budget is most notable in that it has been handed down 21 weeks later than it would normally have been delivered as a direct consequence of the unprecedented chaos and drama caused by the COVID-19 global pandemic. The last time we experienced anything similar was the 1918 flu pandemic (known as the Spanish flu) which was prevalent from February 1918 and lasted until April 1920, infecting around 500 million people (about a third of the world’s population) and leading to between 17 million and 50 million (and by some counts as many as 100 million) deaths worldwide.

For most of 2020, the federal and state governments have had the monumental task of managing the health impacts of the pandemic but particularly in this, his second budget speech, Treasurer Josh Frydenberg’s emphasis was on delivering a budget to provide a road to recovery out of the catastrophic economic black hole caused by the pandemic.

Unlike the catch-cry in the 2019 budget of “return to surplus”, the budget deficit is predicted to hit $213.7 billion and then fall to $66.9 billion by 2023-24, representing 36% of GDP. Total net debt is now expected to reach $703 billion this year and is forecast to peak at a record $966 billion by June 2024. It is expected that the national debt will take over a decade to repay with forecasts dependent on companies confidently hiring and investing for growth, consumers returning to work and spending and on a successful vaccine being developed to combat subsequent waves of infection and allow state borders to open and commerce to flow.

This budget is all about business confidence and jobs – jobs, jobs and more jobs. Recognising that particularly women and young people have been hardest hit with losing their jobs during the turmoil, the Coalition’s mantra of “the best form of welfare is a job” was on display as the Treasurer rolled out a range of spending measures designed to encourage businesses to employ and grow.

The Treasurer announced the JobMaker Hiring Credit which is expected to create 450,000 jobs for young people and will be available for businesses for up to a year. It will give $200 a week to employers who hire workers aged 16-30, and $100 a week for workers aged 30-35. To qualify, new employees must have been on JobSeeker and be given at least 20 hours of work a week with all businesses except the major banks being eligible.

The Government reconfirmed its commitment to the already-announced $1 billion JobTrainer program for school-leavers to provide more low-cost training places and $1.2 billion towards wage subsidies for 100,000 new apprenticeships and traineeships. Also unveiled was the new Women’s Economic Security Statement which provides for $240 million of funding measures over the forward estimates that focus on increasing jobs for women in traditionally male-dominated industries like construction, more co-funded grants for women who fund their own start-ups and a focus on encouraging girls and women to pursue careers in the STEM fields (science, technology, engineering and mathematics).

The big boost for small, medium and large enterprises (with a turnover of less than $5 billion) was $26.7 billion allocated to provide 99% of business with an instant asset write off for 100% of the cost of eligible assets.

For individuals, the measures seek to put money back in people’s pockets with a range of personal tax cuts, an extension to the Low- and Middle-Income Tax Offset (LMITO) and instant cash handouts for pensioners and disability carers who will receive two cash payments of $250 — the first from December 2020 and the second from March 2021.

While it waits for the final report from the Royal Commission into Aged Care Quality and Safety (due next year), the Treasurer announced that older Australians will also benefit from a $1.6 billion spend over the next four years to introduce 23,000 additional home care packages, allowing people the option to remain living at home. He also announced Capital Gains Tax (CGT) relief measures for granny flat arrangements.

More detail on a few of the measures

Personal taxation

The Government has announced $17.8 billion in personal income tax relief to get money back into people’s pockets and support the economic recovery (including $12.5 billion over 2020-21) with the majority of the benefit targeted at those on incomes below $90,000.

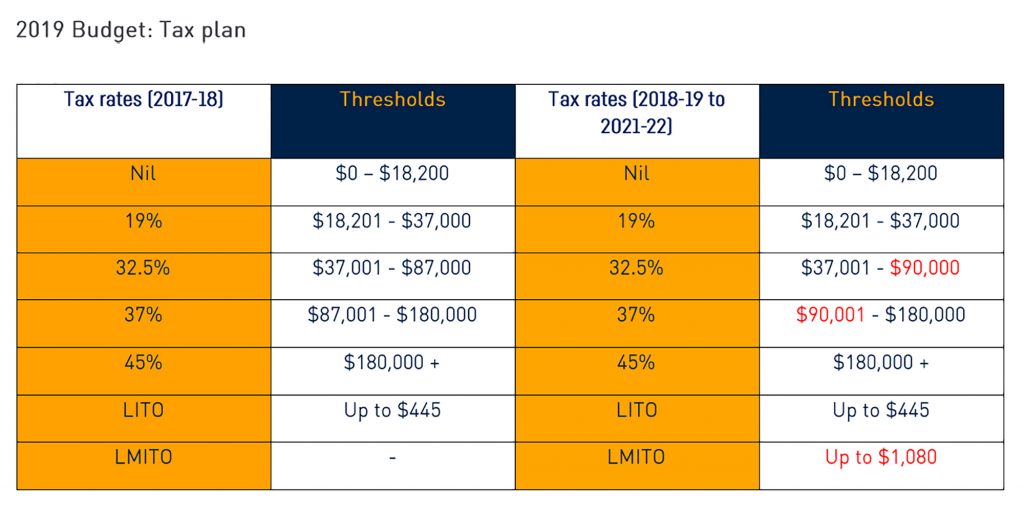

The Government’s three-stage tax plan was announced in 2018 and enhanced in 2019:

- Stage 1 amended the 32.5% and 37% marginal tax brackets over 2018-19 to 2021-22 and introduced the Low- and Middle-Income Tax Offset (LMITO);

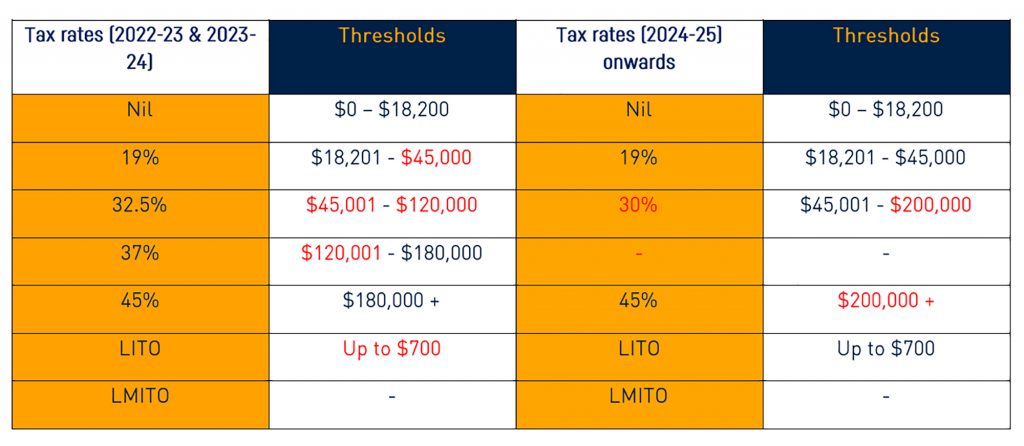

- Stage 2 was designed to further reduce bracket creep over 2022-23 & 2023-24 by amending the 19%, 32.5% and 37% marginal tax brackets; and

- Stage 3 was aimed at simplifying and flattening the progressive tax rates for 2024–25 and increasing the Low-Income Tax Offset (LITO). The Government estimated that around 95 per cent of taxpayers would be on a marginal tax rate of 30% or less (as shown in the tables below).

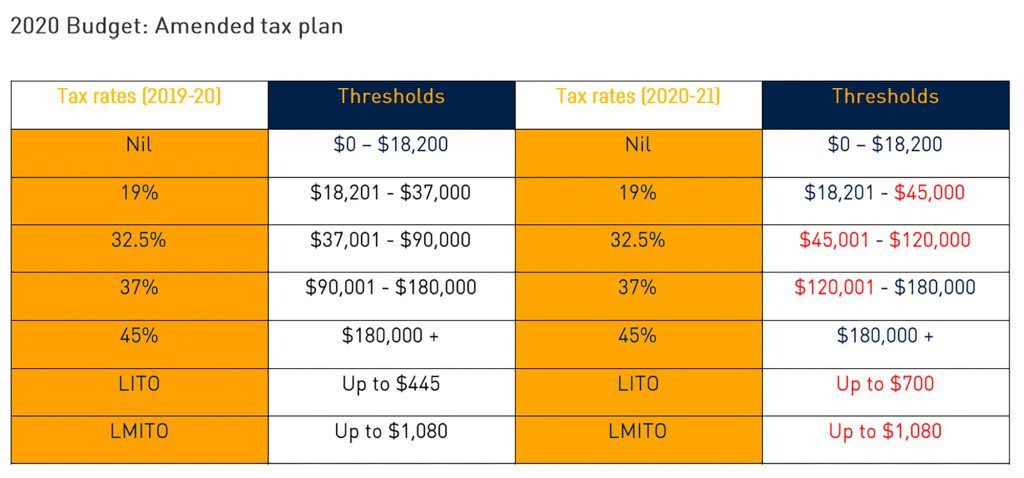

The good news out of this budget is that the Government wants to bring forward the tax cuts from Stage 2 of its plan to begin immediately. The Treasurer announced a 3-stage rollout of the relief such that:

- The low-income tax offset (LITO) will increase from $445 to $700;

- The top threshold of the 19% bracket will increase from $37,000 to $45,000. This will provide up to $1,080 in tax relief; and

- The top threshold of the 32.5% bracket will increase from $90,000 to $120,000. This will provide tax relief of up to $1,350.

If passed, the tax cuts will be back-dated to 1 July 2020, with refunds of withholding tax collected over the last four months to be built into wages until the end of this financial year.

Taxpayers who earn between $45,000 and $90,000 will benefit with an extra $1,080 and those earning more than $90,000 taking home up to $2,565 extra.

From 2024-25, the 3-stage tax plan is still in effect to reduce the 32.5% marginal tax rate to 30% and more closely align the middle tax bracket of the personal income tax system with corporate tax rates. In 2024-25, the entire 37% tax bracket will be abolished under the Government’s already legislated plan. Therefore, with the Government’s announced changes, from 2024-25, there would only be 3 personal income tax rates – 19%, 30% and 45%.

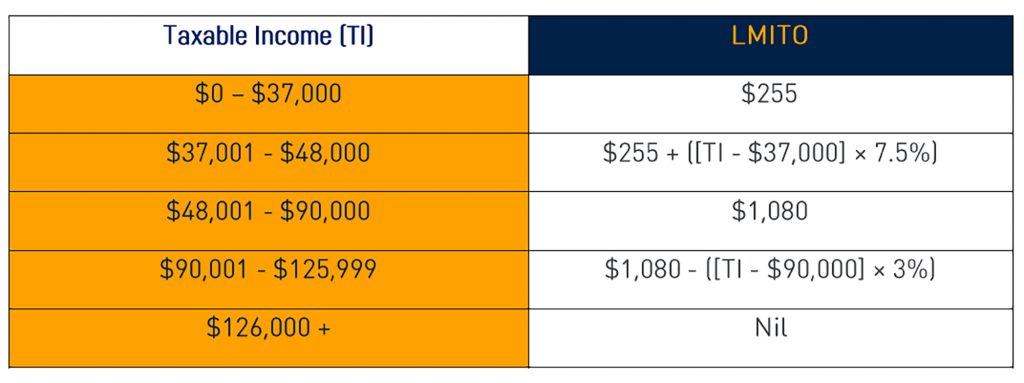

As mentioned, the Government announced it would extend for another year the non-refundable low and middle income tax offset (LMITO). The reduction in tax provided by LMITO will remain at $1,080 per annum ($2,160 for dual-income couples) with the base amount at $255 per annum for the 2020-21 income year.

Superannuation – “stapled” super accounts

Superannuation did not get much of a mention in this year’s budget however the few measures announced were targeted more at the superfunds themselves rather than at members.

The Treasurer noted that Australian’s pay $30 billion a year in super fees and highlighted structural flaws that need addressing. He pointed to unnecessary fees and insurance premiums on multiple accounts, high fees for too many underperforming funds and what he described as a lack of accountability to their members for their conduct and the outcomes they deliver to the members including a lack of transparency on how they spend their members’ money.

The key measure revolves around the concept that a fund “follows” the member, so that a new fund doesn’t need to be opened each time a worker starts a new job. By 1 July 2021, where an employee does not nominate an account at the time they start a new job, employers will need to obtain information about the employee’s existing superannuation fund from the ATO and pay their superannuation contributions to their existing fund.

The Government says that there are currently 6 million super accounts for 4.4 million people costing members $450 million in unnecessary fees. It is expected that consolidating multiple accounts will result in 2.1 million fewer accounts over 10 years and save members an estimated $2.8 billion in duplicated fees, insurance premiums and lost earnings.

The Treasurer announced a new comparison tool called YourSuper, designed to help workers decide which super product will best meets their needs. By 1 July 2021, the YourSuper tool will:

- Provide a table of simple super products (MySuper) ranked by fees and investment returns.

- Link workers to super fund websites where they can choose a MySuper product.

- Show their current super accounts and prompt members to consider consolidating their superfunds if they have multiple accounts.

The Government hopes the ability for members to compare the fees and performance of superfunds will drive competition, reduce cost and improve member outcomes.

In order to hold funds to account for underperformance and to increase accountability and transparency, from 1 July 2021, MySuper products (and from 1 July 2022, other superannuation products) will be subject to an annual performance test and listed on the YourSuper comparison tool as underperforming until they improve.

From 1 July 2021, superfund trustees will also be required to comply with a new duty to act in the best financial interests of their members.

There is no detail on how this measure would be implemented, but under a best interests framework, trustees would need to demonstrate that there was a reasonable basis to support their actions being consistent with members’ best financial interests. Trustees will need to provide members with key information regarding how they manage and spend their money in advance of Annual Members’ Meetings. The Government expects that a reduction in waste in the super system, and improving transparency and accountability, could lead to an increase of $1.1 billion in retirement savings over 10 years.

Social Security and Aged Care

Social security has been in the news for most of this year with the introduction of the JobKeeper and JobSeeker payments to tackle the massive unemployment crisis caused by the economic impacts of the pandemic.

The Government has forecast that unemployment will peak at 8% in the December quarter (2020) but will reduce to 5.5% by 2023-24. And while economic growth is tipped to fall by 3.75% this year, the Government has forecast a sharp turnaround as post-COVID business and consumer confidence kick starts the economic engine with projected growth of 4.75% in 2021/22.

With a strong emphasis on jobs, the Government made no mention of increasing the base rate of the JobSeeker (formerly Newstart) unemployment benefit. The additional coronavirus supplement, currently $250 a fortnight, which is scheduled to end at the end of December, will return the benefit to its pre-pandemic rate. However, Social Services Minister Anne Rushton said there would be more announcements about JobSeeker before the end of the year.

As mentioned, pensioners and disability carers will receive two cash payments of $250 — the first from December 2020 and the second from March 2021.

Specific to retirement living options for older Australians, on top of the announcement of an additional 23,000 home care packages, the Government has announced that it will provide a targeted capital gains tax (CGT) exemption for granny flats (where there is a formal agreement in place). Under the measure, CGT will not apply to the creation, variation or termination of a formal written granny flat arrangement and is designed to address the adverse tax consequences for property owners (where that property is the principal residence of the taxpayer) while providing protection for older parents or people with disabilities.

Business taxation

To add to the solvency reforms to help protect distressed businesses and assist them to work their way through financial hardship and get back to normal operations, the Treasurer announced measures to support small, medium and large businesses with an aggregated annual turnover of less than $5 billion by enabling them to deduct the full cost of eligible depreciable assets. He stated that this measure should help over 99% of businesses to write off the full value of any eligible asset they purchase for their business.

In a measure designed to improve cash flow and to encourage new investment to support the economic recovery, eligible assets (including new depreciable assets and the cost of improvements to existing eligible assets, and for small and medium-sized business, second-hand assets) acquired from 7:30pm (AEDT) on 6 October 2020 and first used or installed by 30 June 2022, can be fully expensed in year of first use.

Further, small businesses can deduct the balance of their simplified depreciation pool at the end of the income year while full expensing applies. Also, businesses that acquired eligible assets under the pre-existing enhanced $150,000 instant asset write-off (IAWO) provisions will have until 30 June 2021 to first use or install those assets.

Conclusion and where to from here?

Unlike the 2019 Budget, the Government has moved from a platform of continued sustainable and responsible economic management and a mantra of “return to surplus” to something much different. The 2020 budget has all the trimmings of a pre-election cash splash, except this is not a pre-election budget. The economic ruin brought about by the worst calamity in the modern age (which has not been a market-driven, debt-driven or geo-political initiated event) has demanded apolitical, bi-partisan action to stave off a potential 1930’s-style depression, so the Government didn’t really have much choice.

Ideological biases aside, a Liberal Coalition government is generally always going to try to create economic activity by appealing to the business community, by creating the economic levers to generate jobs and providing the tax incentives to foster the business and individual confidence to invest and grow. They could always do more and time will tell whether what has been proposed is enough.

As with all budget announcements, the measures are proposals only and need to be enacted by Parliament. This year, the COVID-interrupted sitting dates mean there are limited sitting days for the Government to pass its legislative reforms. The big question is, given it could be a while before many of the measures are enacted, will businesses and individuals have the confidence to start investing and spending to get the economy cranking again?

I urge clients of Infocus to contact your adviser with specific questions.